Quarterly Market Review: April-June 2023

The Markets (second quarter through June 30, 2023)

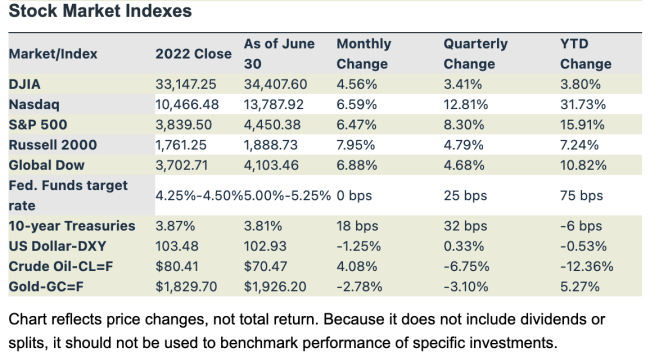

Wall Street proved resilient during the second quarter of the year, despite rising inflation, two interest rate hikes, and concerns about the debt ceiling. The economy remained relatively strong, despite predictions that it may be headed toward a recession. The second quarter saw information technology, communication services, and consumer discretionary account for most of the market gains. Energy, utilities, health care, financials, and consumer staples slid lower. The market's positive performance during the second quarter was buoyed by strength in the labor market, economic data that may be showing inflation is beginning to wane, and a better-than-expected first-quarter gross domestic product.

Government bond yields rose in the second quarter, with investors eyeing the relative strength of the economy as reason to remain bullish on stocks. Each of the benchmark indexes listed here climbed higher in the second quarter, with the Nasdaq enjoying its third-best first half on record, a far cry from last year at this time, when the tech-heavy index was going through its second-worst six-month stretch. The S&P 500 also enjoyed notable growth in the second quarter. The dollar inched higher while gold prices retreated in the second quarter. Notwithstanding a roughly 4.0% increase in June, crude oil prices declined for the fourth consecutive quarter, marking the longest losing streak since 1988. While indications seem to point to a more bullish outlook, crude oil supply continued to outpace demand, muting prices. OPEC+ cuts were offset by production increases from other sources, including the United States. In addition, China's demand has been weaker than anticipated, with manufacturing slow to expand. Prices at the pump rose in the second quarter. The June 26 retail price for regular gasoline was $3.571 per gallon, $0.15 above the March price of $3.421 per gallon. However, gas prices are down $1.301 over the last 12 months.

April began the quarter with stocks posting modest gains from the previous month. The large caps of the Dow (2.5%) and the S&P 500 (1.5%) were bolstered by a rally over the last two days of the month. Small caps declined further with the Russell 2000 falling 1.9%, while remaining marginally ahead of its 2022 year-end value. Among the market sectors in April, industrials underperformed, while communication services fared the best. Data in April showed some signs of economic weakening. Job growth in April (236,000), was well below the monthly average for the year, while the number of workers receiving unemployment insurance reached its highest level since November 2021. Housing data was soft, with the number of residential building permits and housing starts sagging from the previous month. Existing home sales dropped, while the median existing-homes sales price was 0.9% less than a year ago. Financials took a hit after another bank fell into Federal Deposit Insurance Corporation receivership. Despite some economic downturns, other data supported ongoing economic strength and bolstered investor sentiment. First-quarter corporate earnings were somewhat better than expected. The Consumer Price Index inched up only 0.1%, bringing the year-over-year increase to 5.0%, the lowest annual pace since May 2021.

Stocks were mixed in May, with information technology and communication services pushing the Nasdaq up nearly 6.0%, while the Dow lost 3.5%. The S&P 500 inched up 0.3%, but the small caps of the Russell 2000 fell 1.1%. Like the previous month, relatively strong corporate earnings reports and encouraging inflation data helped keep investors in the market. Bond prices slid lower, pushing yields higher, with 10-year Treasuries climbing 18.0 basis points in May. Stocks began the month on a downturn after the Federal Reserve hiked interest rate 25.0 basis points, while giving no clear indication as to whether or when more rate hikes were coming. For much of the month, investors focused on the debt ceiling negotiations between President Biden and House Speaker McCarthy. Mega-cap technology and artificial intelligence stocks dominated the market for much of May. Inflation remained elevated, with the personal consumption expenditures price (PCE) index, a preferred inflation indicator of the Federal Reserve, rising 4.3% for the year, while consumer prices excluding food and energy rose 4.7%.

June was a strong month for stocks, with each of the benchmark indexes listed here posting gains of between 4.6% and 8.0%. Inflationary pressures showed signs of cooling, with the 12-month PCE price index coming in at 3.8%. The Consumer Price Index rose 4.0% for the year, the smallest 12-month increase since the comparable period ended March 2021. The Federal Reserve elected not to increase interest rates in June, opting, instead, to step back and assess additional information and its implications for monetary policy. Gross domestic product advanced at a stronger-than-expected 2.0% for the first quarter, showing resilience in the economy. Despite the collapse of several major U.S. banks, the Federal Reserve indicated that the largest domestic banks are sufficiently positioned to continue lending to households and businesses even during a severe recession. The labor market picked up the pace, adding nearly 340,000 new jobs, in line with the average monthly gain over the past 12 months. Industrial production declined minimally, following two consecutive monthly increases. While manufacturing slowed, business activity in the services sector expanded at the fastest rate since April 2022. Long-term bond yields increased in June from May, as bond prices dipped lower.

Latest Economic Reports

- Employment: Employment rose by 339,000 in May from April, in line with an average monthly gain of 341,000 over the prior 12 months. In May, employment continued to trend upward in professional and business services, health care, government, construction, transportation and warehousing, and social assistance. The unemployment rate rose 0.3 percentage point to 3.7%. In May, the number of unemployed persons rose by 440,000 to 6.1 million. The employment-population ratio, at 60.3%, and the labor force participation rate, at 62.6%, were little changed from the previous month. Both measures have shown little net change since early 2022. In May, average hourly earnings increased by $0.11, or 0.3%, to $33.44. Over the past 12 months ended in May, average hourly earnings rose by 4.3%. The average workweek edged down 0.1 hour to 34.3 hours.

- There were 239,000 initial claims for unemployment insurance for the week ended June 24, 2023. The total number of workers receiving unemployment insurance was 1,742,000. By comparison, over the same period last year, there were 213,000 initial claims for unemployment insurance, and the total number of claims paid was 1,340,000.

- FOMC/interest rates: The Federal Open Market Committee maintained the federal funds target range rate at the current 5.00%-5.25% in June. The Committee essentially decided to assess the effects of prior rate increases. However, the FOMC indicated that more rate hikes are likely, noting that inflation remained elevated, while economic activity expanded at a modest pace and job gains have been robust. Overall, the FOMC will base its decisions on available data, and "will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments." The summary of economic projections has the federal funds rate at 5.6% in June from 5.1% in March, which suggests the fed interest rate will be increased by 50.0 basis points by the end of 2023.

- GDP/budget:Economic growth slowed minimally in the first quarter, as gross domestic product increased 2.0%, according to the third and final estimate from the Bureau of Economic Analysis. GDP rose 2.6% in the fourth quarter. The deceleration in first-quarter GDP compared to the previous quarter primarily reflected downturns in private inventory investment and residential fixed investment. Consumer spending, as measured by personal consumption expenditures, rose 4.2% in the first quarter compared to a 1.0% increase in the fourth quarter. Consumer spending on long-lasting durable goods jumped 16.3% in the first quarter after decreasing 1.3% in the prior quarter. Spending on services rose 3.2% (1.6% in the fourth quarter). Nonresidential fixed investment increased 0.6% after climbing 4.0% in the fourth quarter. Residential fixed investment fell 4.0% in the first quarter, significantly better than the 25.1% decrease in the fourth quarter. Exports increased 7.8% in the first quarter, following a decrease of 3.7% in the fourth quarter. Imports, which are a negative in the calculation of GDP, increased 2.0% in the first quarter after declining 5.5% in the previous quarter. Consumer prices increased 4.1% in the first quarter compared to a 3.7% advance in the fourth quarter. Excluding food and energy, consumer prices advanced 4.9% in the first quarter (4.4% in the fourth quarter).

- The federal budget had a $240.3 billion deficit in May, well above the May 2022 deficit of $66.2 billion. The deficit for the first eight months of fiscal year 2023, at $1,164.9 trillion, is much higher than the $426.2 billion deficit over the same period of the previous fiscal year. In May, government receipts totaled $307.5 billion for the month and $3.0 trillion for the current fiscal year. Government outlays were $547.8 billion in May and $4.2 trillion through the first eight months of fiscal year 2023. By comparison, receipts in May 2022 were $389.0 billion and $3.4 trillion through the first eight months of the previous fiscal year. Expenditures were $455.2 billion in May 2022 and $3.8 trillion through the comparable period in FY22.

- Inflation/consumer spending: According to the latest Personal Income and Outlays report, the personal consumption expenditures price index edged up 0.1% in May and 3.8% since May 2022. Prices excluding food and energy advanced 0.3% in May, following increases of 0.4% in April and 0.3% in March. Prices for goods decreased 0.1%, while prices for services increased 0.3%. Food prices increased 0.1% and energy prices decreased 3.9%. Since May 2022, consumer prices for food increased 5.8%, while energy prices declined 13.4%. Personal income rose 0.4% in May, 0.1 percentage point greater than the April increase. Disposable personal income increased 0.4% in May after advancing 0.3% in April. Consumer spending increased 0.1% in May, after rising 0.6% in the previous month.

-

The Consumer Price Index rose 0.1% in May after increasing 0.4% in April. Over the 12 months ended in May, the CPI advanced 4.0%, down from 4.9% for the year ended in April. Excluding food and energy prices, the CPI rose 0.4% in May and 5.3% over the last 12 months. Contributing to the May CPI advance were increases in prices for shelter (0.6%) and used cars and trucks (4.4%). In May, food prices increased 0.2% and 6.7% since May 2022. Energy prices fell 3.6% in May and are down 11.7% over the 12 months ended in May.

-

Prices that producers received for goods and services decreased 0.3% in May, following a 0.2% increase in the previous month. Producer prices increased 1.1% for the 12 months ended in May. The Producer Price Index saw prices for goods fall 1.6%, while prices for services increased 0.2%. Producer prices less foods, energy, and trade services were unchanged in May after increasing 0.1% in the previous month. Prices less foods, energy, and trade services advanced 2.8% for the year ended in May after increasing 3.3% from the 12 months ended in April.

- Housing: Sales of existing homes increased 0.2% in May. Since May 2022, existing-home sales dropped 12.7%. According to the report from the National Association of Realtors®, job gains, a dearth of inventory, and fluctuating mortgage rates have contributed to the decline in sales of existing homes. The median existing-home price was $396,100 in May, up from $385,900 in April but lower than the May 2022 price of $408,600. In May, unsold inventory of existing homes represented a 3.0-month supply at the current sales pace, up from the April pace of 2.9 months. Sales of existing single-family homes dropped 0.3% in May and 20.0% from May 2022. The median existing single-family home price was $401,100 in May, up from the April price of $390,200 but well below the May 2022 price of $415,400.

- New single-family home sales advanced in May, climbing 12.2%, marking the third consecutive monthly increase. Sales were up 20.0% from a year earlier. The median sales price of new single-family houses sold in May was $416,300 ($402,400 in April). The May average sales price was $487,300 ($495,600 in April). The inventory of new single-family homes for sale in May decreased to 6.7 months, down from 7.6 months in April.

- Manufacturing: Industrial production declined 0.2% in May after increasing 0.5% the previous month. Manufacturing increased 0.1% in May, bolstered by 0.3% increase in durables, which was offset by a 0.1% decrease in noondurables. In May, mining fell 0.4%, while utilities dropped 1.8%.The decrease in mining was driven primarily by decreases in coal mining and support activities (in particular, oil and gas well drilling).The output of utilities declined for the second consecutive month, as electric utilities fell in May, while natural gas utilities remained unchanged. Total industrial production in May was 0.2% above its year-earlier level. Major market groups posted mixed results in May. Notable gains were recorded in defense and space equipment and construction supplies. Most other major market groups recorded modest declines.

- New orders for durable goods increased 1.7% in May after increasing 1.2% in April. New orders for transportation equipment led the overall increase, advancing 3.9% in May, marking the third consecutive monthly advance. Excluding transportation, new orders increased 0.6% in May. Excluding defense, new orders rose 3.0%. Over the past 12 months, new orders for durable goods have increased 3.5%.

- Imports and exports: May saw both import and export prices decrease. Import prices fell 0.6%, following a 0.3% increase in April. Prices for imports declined 5.9% over the past year, the largest 12-month drop since the index declined 6.3% for the 12 months ended in May 2020. Import fuel prices decreased 6.4% in May, following a 4.1% jump in April. The May decline in import fuel prices was the largest monthly drop since August 2022. Nonfuel import prices edged down 0.1% in May after being unchanged in the previous month. Lower prices in May for nonfuel industrial supplies and materials and foods, feeds, and beverages more than offset higher prices for automotive vehicles and capital goods. Nonfuel import prices declined 1.6% over the past year. Export prices dropped 1.9% in May, the largest monthly decrease since December 2022. Falling prices for both agricultural and nonagricultural exports contributed to the overall decline in export prices in May. Export prices fell 10.1% for the year ended in May, the largest 12-month decline since the series was first published in September 1984.

- The international trade in goods deficit fell $6.0 billion, or 6.1%, in May over April. Exports of goods for May were $1.0 billion, or 0.6%, below April exports. Imports of goods were $6.9 billion, or 2.7%, less than April imports. The May decrease in exports was mainly attributable to declines in other goods (-13.2%) and foods, feeds, and beverages (-14.2%). The decrease in May imports was largely driven by a 7.3% decline in consumer goods.

- The latest information on international trade in goods and services, released June 7, was for April and revealed that the goods and services trade deficit was $74.6 billion, an increase of 23.0% from the March deficit. April exports were $249.0 billion, 3.6% less than March exports. April imports were $323.6 billion, 1.5% above March imports. For the 12 months ended in April, the goods and services deficit decreased 23.9%. Exports increased 5.8%, while imports decreased 2.3%.

- International markets: China's post-pandemic economic recovery showed new signs of weakness in June. Manufacturing in China contracted for the third straight month in June, while the services sector also weakened. The latest data likely prompted the Chinese government to lower the one-year loan prime rate by 10 basis points. With inflationary pressures continuing to rise, the Bank of England hiked interest rates by 50 basis points in June, marking the 13th consecutive interest rate increase. Elsewhere, in Germany, manufacturing declined in both goods and services sectors. What was often the fulcrum of the German economy, weak global demand has impacted German exports. For June, the STOXX Europe 600 Index was flat; the United Kingdom's FTSE slid 0.8%; Japan's Nikkei 225 Index gained 5.3%; and China's Shanghai Composite Index dipped 0.9%.

- Consumer confidence: The Conference Board Consumer Confidence Index® increased in June to 109.7, up from a revised 102.5 in May. The Present Situation Index, based on consumers' assessment of current business and labor market conditions, rose to 155.3 in June, higher than the May reading of 148.9. The Expectations Index, based on consumers' short-term outlook for income, business, and labor market conditions, advanced to 79.3 in June from 71.5 in May. According to the Conference Board's report, the Expectations Index has remained below 80.0, the level associated with a recession within the next year, since February 2022, with the exception of a brief uptick in December 2022. However, June's reading was just a shade below 80.0 and up sharply from prior month's rate.

Eye on the Quarter Ahead

During the third quarter, investors will likely focus on inflation data and the Federal Reserve's response. Concerns over slowing economic activity, both here and globally, also will influence the market going forward.

Data sources: Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services). Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/Bloomberg.com Market Data (oil spot price, WTI Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates). News items are based on reports from multiple commonly available international news sources (i.e., wire services) and are independently verified when necessary with secondary sources such as government agencies, corporate press releases, or trade organizations. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities, and should not be relied on as financial advice. Forecasts are based on current conditions, subject to change, and may not come to pass. U.S. Treasury securities are guaranteed by the federal government as to the timely payment of principal and interest. The principal value of Treasury securities and other bonds fluctuates with market conditions. Bonds are subject to inflation, interest-rate, and credit risks. As interest rates rise, bond prices typically fall. A bond sold or redeemed prior to maturity may be subject to loss. Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful.

The Dow Jones Industrial Average (DJIA) is a price-weighted index composed of 30 widely traded blue-chip U.S. common stocks. The S&P 500 is a market-cap weighted index composed of the common stocks of 500 largest, publicly traded companies in leading industries of the U.S. economy. The NASDAQ Composite Index is a market-value weighted index of all common stocks listed on the NASDAQ stock exchange. The Russell 2000 is a market-cap weighted index composed of 2,000 U.S. small-cap common stocks. The Global Dow is an equally weighted index of 150 widely traded blue-chip common stocks worldwide. The U.S. Dollar Index is a geometrically weighted index of the value of the U.S. dollar relative to six foreign currencies. Market indexes listed are unmanaged and are not available for direct investment.

IMPORTANT DISCLOSURES

Philippe E Berthoud and William E. Riquier offer Securities and Advisory Services through United Planners Financial Services, Member FINRA/SIPC. United Planners and The Retirement Financial Center are independent companies.

Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, legal, or retirement advice or recommendations. The information presented here is not specific to any individual's personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable — we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

This communication is strictly intended for individuals residing in the state(s) of AZ, CA, CO, CT, FL, GA, ME, MD, MA, MT, NV, NH, NJ, NY, VA and WA. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2023.