ANNUAL MARKET REVIEW 2019

Overview

The year began with the government stymied by a shutdown, and ended with articles of impeachment levied against the president. In between, both domestic and global economies showed signs of slowing, all while the trade war between the United States and China loomed throughout the year. Nevertheless, investors remained relatively bullish toward stocks, pushing several major indexes to record highs.

While domestic economic growth may have slowed in 2019 compared to 2018, it showed resilience and stamina. The third-quarter gross domestic product expanded at an annualized rate of 2.1% — moderately down from 2018's 3.0% rate, yet still strong enough to outpace global economic growth by a considerable margin. Consumer spending — which accounts for about two-thirds of the U.S. economy — surged, buoyed by a strong labor market, near-record unemployment, solid wage growth, and a burgeoning stock market. All told, the domestic economic expansion continued into its 11th straight year, the longest run in U.S. history.

Last year saw trade disputes between the United States and several of its trade partners reach an accord, but the trade war with China roared. The world's two largest economies engaged in a tit-for-tat skirmish, with each country volleying tariffs on their respective imports at the expense of the exporting nation. Coincidentally, a limited deal was announced just before the holiday shopping season, with the U.S. agreeing to forgo new tariffs and China assenting to allow more U.S. agricultural imports. Further negotiations are presumed, but the relationship between the economic giants remains tenuous at best.

Not only did the ongoing trade war affect global economies, but it also impacted domestic business investment, industrial production, and exports. Part of the justification cited by the Federal Reserve for lowering interest rates three times last year was weakness in business fixed investment and exports. As of November, new orders for durable goods were down 1.3% from the same period in 2018, and business (nonresidential) investment fell 2.3% in the third quarter.

The new year begins with a strong stock market and solid economic growth. The Secure Act, passed in late December, should change the retirement planning (and saving) landscape to some extent. However, the Treasury budget deficit for fiscal 2019 (October 2018-September 2019) exceeded $980 billion — 26% higher than the 2018 fiscal-year deficit. The trade war with China may cool with more mutual concessions, or accelerate, which would continue to dampen global economic growth. The new year will begin with the impeachment process and end with November's presidential election. What happens in between is anyone's guess. Will unemployment and inflation remain low? Will stocks continue to experience growth? Will oil and gas prices moderate or surge? Will the domestic economy continue to accelerate, or suffer a setback? Can the world economy recover, or will it continue to stagnate? If nothing else, 2020 looks to be an interesting year.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Snapshot 2019

The Markets

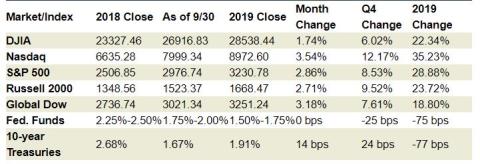

- Equities: The year 2019 was a solid one for investors. A year after one of the worst fourth quarters since the Great Recession, stocks rebounded to close 2019 with several major indexes reaching record highs. During the year, investors faced a yield curve inversion for the first time since 2007, a slowing economy, and a constant barrage of positive and negative information on the trade war with China. Nevertheless, investors stayed the course for most of the year, pushing stocks to their best year since 2013.

- Each of the benchmark indexes listed here closed 2019 in fine fashion, led by the tech stocks of the Nasdaq, which gained more than 35.0%. The large caps of the Dow (23.34%) and the S&P 500 (28.88%) also fared well by year's end. The small caps of the Russell 2000 began the year on a tear, ending February up almost 17.0%. However, the small-cap benchmark index pulled back some in March but remained a steady gainer for much of the rest of the year, closing 2019 about 24.0% ahead of where it started. The Global Dow gained about 19.0% on the year despite ongoing Brexit turmoil, frequent terrorist attacks, and overall global economic weakening.

- Bonds: U.S. Treasury yields swung dramatically in 2019, ranging from a low of 1.43% to a high of 2.80%. Investors were a bit unnerved in March when a recession indicator — an inverted yield curve — occurred for the first time since 2007. That's what happened when the yield on U.S. 10-year Treasuries fell below the yield on the 3-month note — a potential sign of an economic slowdown. However, the yield inversion was short-lived. Investors saw a steadying economy, modest inflationary pressures, and continued job growth, all of which helped ease investor concerns. Overall, the yield on 10-year Treasuries closed at 1.91%, about 77 basis points below where it began the year, as rising bond prices dragged yields lower (bond yields move in the opposite direction from bond prices).

- Oil: Oil prices began 2019 at $46.54 per barrel and continued pushing higher, reaching a peak price of $66.60 per barrel in April. During the year, oil prices fell in the summer months, averaging about $54 per barrel. Oil prices spiked nearly 20% in September, reaching almost $63 per barrel, only to fall back again in October. Since then, prices have climbed steadily to their year-end price of $61.21 per barrel. Ultimately, oil prices closed 2019 with their largest yearly gain since 2016. WTI crude has climbed nearly 36% from its January opening price.

- FOMC/interest rates: The Federal Open Market Committee lowered interest rates three times during 2019 after raising them four times in 2018. Each time the target range decreased by 25 basis points. The first rate drop occurred in July, followed by a rate decrease in September and a final cut in October. The Committee left rates unchanged following its last meeting for 2019 in December. For the year, the target range has decreased 75 basis points, from 2.25%-2.50% to 1.50%-1.75%. Following each rate increase, the Committee noted that inflation continued to run below the Committee's target 2.0% rate, business fixed investment and exports weakened, and global economic developments were uncertain. Nevertheless, the overall view of the economy is favorable, and a higher bar will have to be met before further rate reductions are suggested.

- Currencies: The dollar maintained a relatively strong position throughout much of 2019. The United States Dollar Index, or DYX, which measures the U.S. dollar against the currencies of several other countries, ranged from a low of $95.02 to a high of $99.67, ultimately closing 2019 at $96.92.

- Gold: Gold prices rose over 18% in 2019. Gold prices began the year at $1,278.30 on January 1. Prices hit a low in May of $1,267.30 to a high in September of $1,566.20. The price of gold closed 2019 at $1,520.00.

Last Month's Economic News

- Employment: The unemployment rate inched down 0.1 percentage point to 3.5% in November as the number of unemployed persons dipped from 5.86 million in October to 5.81 million in November. Total employment rose by 266,000 in November after adding 156,000 (revised) new jobs in October. The average monthly job gain through November is 180,000 (223,000 in 2018). Notable employment increases for November occurred in manufacturing (54,000), health care (45,000), professional and technical services (31,000), leisure and hospitality (45,000), and transportation and warehousing (16,000). The labor participation rate fell 0.1 percentage point to 63.2%, and the employment-population ratio remained at 61.0%. The average workweek remained at 34.4 hours for November. Average hourly earnings rose by $0.07 to $28.29. Over the last 12 months ended in November, average hourly earnings have risen 3.1%.

- FOMC/interest rates: The Federal Open Market Committee met in December for the first time since October. After dropping interest rates for the third time this year in October, the Committee elected to maintain rates at their current target range of 1.50%-1.75%. The Committee next meets January 28-29.

- GDP/budget: According to the third and final estimate for the third-quarter gross domestic product, the economy accelerated at an annualized rate of 2.1%, up from the second quarter's 2.0% annual growth rate. The first quarter saw an annualized growth of 3.1%. Growth in consumer spending (personal consumption expenditures), which accounts for roughly two-thirds of the GDP, slowed from 4.6% in the second quarter to 3.2%. Gross domestic income increased 2.1% in the third quarter, compared with an increase of 0.9% in the second quarter. The personal consumption expenditures price index increased 1.5% in the third quarter. November saw the federal budget deficit grow to $208.8 billion, $74.0 billion over October's deficit. The government spent roughly $434.0 billion in November and had receipts of $225.2 billion. Most of the government outlays were for Social Security ($89 billion), Medicare ($83 billion), and national defense ($63 billion). Individual income taxes accounted for the majority of receipts ($106 billion), followed by social insurance and retirement receipts ($97 billion). Corporate income taxes accounted for a little over $0.5 billion.

- Inflation/consumer spending: According to the Personal Income and Outlays report, inflationary pressures remain weak, as prices for consumer goods and services rose 0.2% in November, the same increase as in October. Prices are up 1.5% over the last 12 months. Consumer prices excluding food and energy rose 0.1% in November (0.1% in October) and are up 1.6% year-over-year. Personal income and disposable (after-tax) personal income each advanced 0.5% ahead of October's respective figures. Consumers continued to spend, as personal consumption expenditures increased 0.4% in November after expanding 0.3% the previous month.

-

The Consumer Price Index climbed 0.3% in November following a 0.4% increase in October. Over the 12 months ended in November, the CPI rose 2.1%. Increases in shelter and energy were major factors in the CPI increase. Energy prices increased 0.8% on the month with gasoline up 1.1%. Prices less food and energy rose 0.2% in November, the same increase as in October. Since last October, core prices (less food and energy) are up 2.3%.

-

Prices producers receive for goods and services rose 0.4% in November following a similar October jump. The index increased 1.1% for the 12 months ended in November. Producer prices less foods, energy, and trade services was unchanged in November after inching up 0.1% in October. For the 12 months ended in November, prices less foods, energy, and trade services moved up 1.3%, the smallest advance since climbing 1.3% in the 12 months ended September 2016. Prices for goods rose 0.3% in November while prices for services edged down 0.3%.

- Housing: The housing sector has been anything but consistent this year. After rising 1.9% in October, sales of existing homes dropped 1.7% in November. Year-over-year, existing home sales are up 2.7%. Existing home prices advanced in November to a median price of $271,300, compared to $270,900 in October. Existing home prices were up 5.4% from November 2018. Total housing inventory at the end of November sat at 1.64 million units (representing a 3.7-month supply), down from October's 3.9% inventory rate. After falling 0.7% in October, sales of new single-family home advanced 1.3% in November, and are 16.9% above the November 2018 estimate. The median sales price of new houses sold in November was $330,800 ($316,700 in October). The average sales price was $388,200 ($383,300 in October). Available inventory, at a 5.4-month supply, remained about the same in November as it was in October.

- Manufacturing: Industrial production and manufacturing production both rebounded 1.1% in November after declining in October. These sharp November increases were largely due to a bounce back in the output of motor vehicles and parts following the end of a strike at a major manufacturer. Excluding motor vehicles and parts, the indexes for total industrial production and for manufacturing moved up 0.5% and 0.3%, respectively. In November, mining output fell 0.2% (-0.7% in October), while utilities increased 2.9% after falling 2.4% in October. Total industrial production was 0.8% lower in November than it was a year earlier. Following an October increase, new orders for durable goods fell 2.0% in November. Excluding transportation, new orders were virtually unchanged. Excluding defense, new orders expanded by 0.8%. Helping drive the decrease in durable goods orders were retractions in defense aircraft and parts (-72.7%), nondefense aircraft and parts (-1.8%), machinery (-1.6%), and transportation equipment (-5.9%). New orders for capital goods (used by businesses to produce consumer goods) dropped 7.8% in November after climbing 3.8% in October.

- Imports and exports: Both import and export prices inched higher in November. Import prices rose 0.2% after falling 0.5% in the prior month, an increase largely driven by higher fuel prices. Import prices excluding fuel dropped 0.1% in November. Import prices declined 1.3% from November 2018 to November 2019. The 12-month decrease was the smallest over-the-year decline since the index fell 0.9% during the 12-month period ended May 2019. Export prices advanced 0.2% in November after declining 0.1% in October. Overall, export prices dipped 1.3% over the past year. Agricultural export prices rose 2.2% in November, while nonagricultural prices for items such as consumer goods, automobiles, and industrial supplies and materials were unchanged, but are down 1.6% during the 12 months ended in November. The latest information on international trade in goods and services, out December 5, is for October and shows that the goods and services deficit was $47.2 billion, $3.9 billion less than September's revised $51.1 billion deficit. October exports were $0.4 billion less than September exports. October imports were $4.3 billion under September imports. Year-to-date, the goods and services deficit increased $6.9 billion, or 1.3%, from the same period in 2018. Exports decreased less than 0.1%. Imports increased 0.2%. The advance report on international trade in goods (excluding services) revealed the trade deficit fell to its lowest level in three years in November. The international trade deficit was $63.2 billion in November, down $3.6 billion from $66.8 billion in October. Exports of goods for November were $136.4 billion, $0.9 billion more than October exports. Imports of goods for November were $199.6 billion, $2.7 billion less than October imports.

- International markets: British Prime Minister Boris Johnson's Conservative Party scored a resounding electoral victory in last month's parliamentary elections, likely securing Britain's exit from the European Union. The gross domestic product for Great Britain rose 0.4% in the third quarter, lifting the annual economic expansion to 1.1%. In what is claimed as support for more open trade globally, China agreed to cut import tariffs on frozen pork, pharmaceuticals, and some high-tech components beginning January 1, 2020.

- Consumer confidence: Consumer confidence fell again in December for the second consecutive month. The Conference Board Consumer Confidence Index® registered 125.5 in December, down from 126.8 in November. The Present Situation Index — based on consumers' assessment of current business and labor market conditions — increased from 166.6 to 170.0. The Expectations Index — based on consumers' short-term outlook for income, business and labor market conditions — decreased from November's 100.3 to 97.4 in December.

Eye on the Year Ahead

Economic growth slowed in 2019, but not enough to prompt investors to avoid stocks. Fears of a global economic slowdown continuing into 2020 may affect the U.S. economy as well. The housing market hasn't picked up the pace and is generally lagging behind other economic mainstreams. Ongoing global trade negotiations between the United States and China should bode well for the U.S. and global economies. Ultimately, our economy, equity markets, and standing in the world depends on the outcome of the impeachment proceedings and November's presidential election.

Data sources: Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services). Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/Bloomberg.com Market Data (oil spot price, WTI Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates). News items are based on reports from multiple commonly available international news sources (i.e. wire services) and are independently verified when necessary with secondary sources such as government agencies, corporate press releases, or trade organizations. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities, and should not be relied on as financial advice. Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful.

The Dow Jones Industrial Average (DJIA) is a price-weighted index composed of 30 widely traded blue-chip U.S. common stocks. The S&P 500 is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. The NASDAQ Composite Index is a market-value weighted index of all common stocks listed on the NASDAQ stock exchange. The Russell 2000 is a market-cap weighted index composed of 2,000 U.S. small-cap common stocks. The Global Dow is an equally weighted index of 150 widely traded blue-chip common stocks worldwide. The U.S. Dollar Index is a geometrically weighted index of the value of the U.S. dollar relative to six foreign currencies. Market indices listed are unmanaged and are not available for direct investment.

To find out more click here

| Refer a friend |

|

IMPORTANT DISCLOSURES Philippe E Berthoud and William E. Riquier offer Securities and Advisory Services through United Planners Financial Services, Member FINRA/SIPC. United Planners and The Retirement Financial Center are independent companies. Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, legal, or retirement advice or recommendations. The information presented here is not specific to any individual's personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable — we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice. This communication is strictly intended for individuals residing in the state(s) of AZ, CA, CO, CT, FL, GA, ME, MD, MA, MT, NV, NH, NJ, NY, VA and WA. No offers may be made or accepted from any resident outside the specific states referenced. |

|

|

Prepared by Broadridge Advisor Solutions Copyright 2020. To opt-out of future emails, please click here. |